The storm gradually subsided! The final scale of primary aluminum billets production cuts in July was lower than expected, with a smooth resumption pace in August. Three main reasons contributed to this: (1) Aluminum prices hovered at highs during the off-season, and the adaptability of the industry chain to high aluminum prices strengthened; (2) Aluminum smelters adopted a clear stance, leaving limited room for aluminum billet producers to halt or cut production; (3) After the production cut turmoil, the center of processing fees slightly rose, easing financial pressure on aluminum billet enterprises.

Looking back at the earlier production cut turmoil, it started with marginal cuts in early June, escalated into regional large-scale halts and reductions by late June and early July, and continued to expand slightly until mid-July. Only in late July did some billet plants choose to resume production, while August overall saw a smooth resumption pace. The daily average production of primary aluminum billets in July decreased by 4,000 mt MoM to around 45,000 mt/day but remained slightly higher than the expected 44,000 mt/day. August’s daily average production is expected to rebound to 47,000 mt/day.

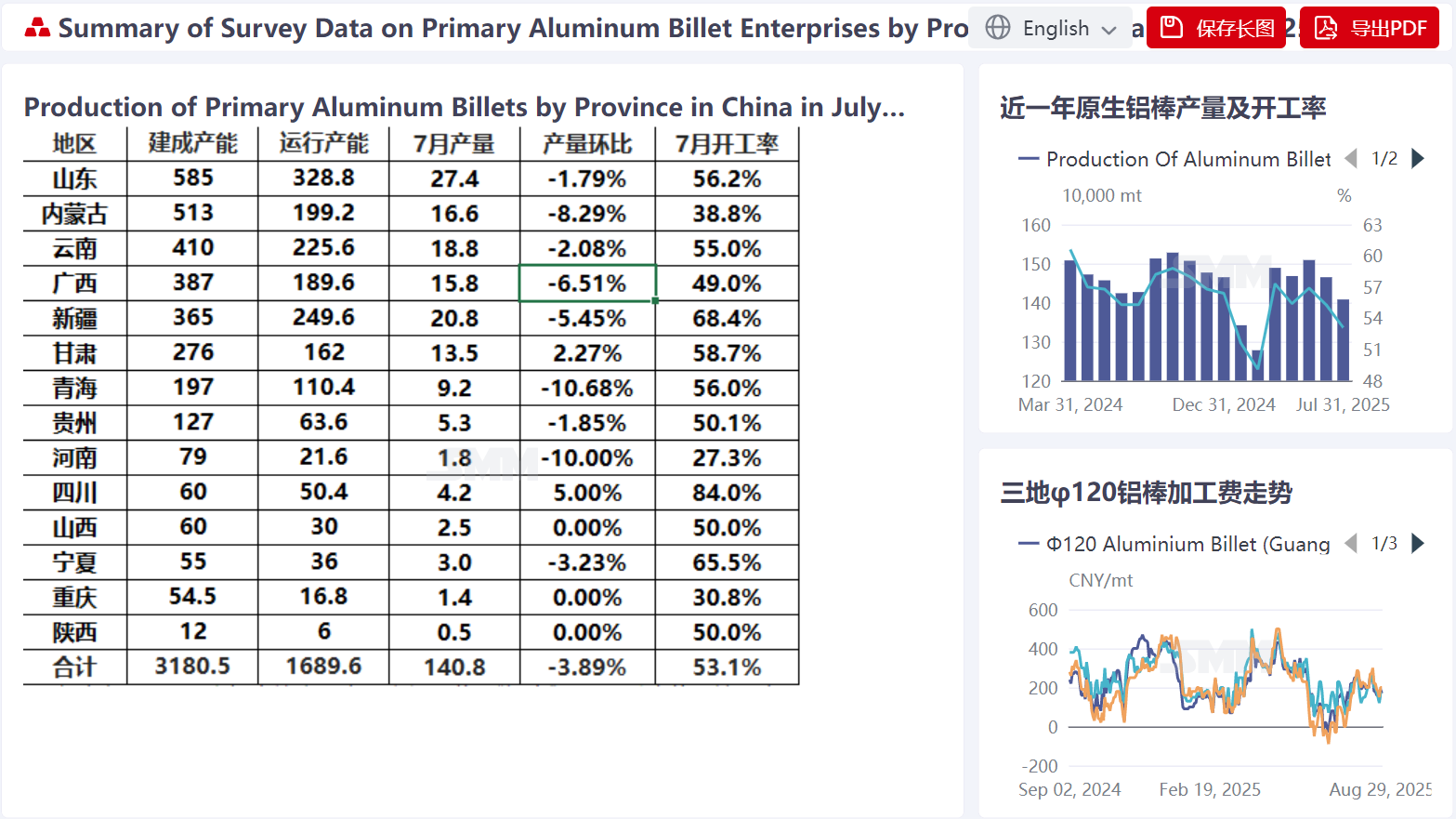

First, examining the final statistics of July’s aluminum billet production cuts: According to the SMM monthly survey, the current sample covers 173 enterprises with a total capacity of 31.805 million mt, flat MoM. In July 2025 (31 days), China’s total primary aluminum billet production was 1.408 million mt, down 57,000 mt (3.9%) MoM from June 2025 (30 days) and down 19,000 mt (1.3%) YoY. The operating rate for primary aluminum billets in July was 53.1%, down 2.2% MoM. Regionally, Qinghai, Henan, Inner Mongolia, Guangxi, and Xinjiang saw the largest production declines due to expanded cuts, while Shandong, Yunnan, Guizhou, and Ningxia experienced relatively controllable reductions. Meanwhile, Gansu and Sichuan bucked the trend with rising production. Final statistics show that July’s actual output exceeded expectations by 44,000 mt, and the operating rate was 1.3% higher than expected, indicating a smaller-than-anticipated scale of production cuts.

What about August’s production forecast? Has full resumption been achieved? Based on SMM’s latest survey of aluminum billet enterprises across provinces (after desensitization), August’s (31 days) primary aluminum billet production is estimated at 1.462 million mt, up 54,000 mt (3.8%) MoM from July 2025, with the operating rate rebounding 2.1% to 55.2%. However, it was down 51,000 mt (3.8%) YoY. As the aluminum billet market stabilized in August, most provinces saw production rebound, except for Gansu and Chongqing, where output dipped slightly due to minimal earlier cuts. Inner Mongolia, Yunnan, Guangxi, Qinghai, Sichuan, and Shanxi are expected to post growth exceeding 5%.

By late August, SMM learned that some previously halted or reduced aluminum billet enterprises in south-west China (e.g., Yunnan and Guangxi) had completed maintenance and resumed production smoothly, driving a weekly operating rate rebound. SMM survey data show that late August’s in-plant aluminum billet inventory stood at 93,000 mt, down 22,000 mt MoM, with average days of inventories dropping 0.4 day to 1.9 days. SMM expects that recent destocking (in-plant and social inventories) signals a clear recovery in market consumption, indicating the off-season has largely passed. However, outflows from warehouses suggest the peak season has yet to arrive, and end-user demand must still drive consumption. Aluminum billet processing fees are expected to remain below 300 yuan/mt in the short term, potentially breaking the 300-yuan threshold after the peak season returns.

(Note: August production data are forecasts. Data source disclaimer: Except for publicly available information, other data are derived from public information, market exchanges, and SMM’s internal database model, processed by SMM for reference only and not constituting decision-making advice.)